As developments in technology and commerce accelerate at rapid speeds, we’ve gone from physically shopping in-store, to mail orders via telephone, to digital online orders at the touch of a button in a relatively short space of time. Now, retailers and services are targeting consumers on their commutes.

“In-car commerce” is the latest way to shop, with advances in on-board technology making this new commerce opportunity viable for the micro insurance industry to innovate within.

In this article, we take a look at how connected cars enable micro insurance and consider a few examples of how micro insurance incident protection can be used to provide a safety net and improve the driving experience.

Getting connected.

Connected-cars have been around since the mid 90’s, and have been evolving ever since. General Motors (GM) was the first manufacturer to develop an interactive in-car communications system. Their web-based OnStar technology enabled Cadillac drivers in the US and Canada to lock and unlock their doors from remote locations and connect to emergency operators, providing convenient security, safety, and roadside assistance features. Fast forward a decade and connected roadside assistance was still being showcased in the latest Hollywood blockbusters, with BMW’s connected ‘Assist’ featuring after a collision in Die Hard 4.

Nearly 30 years on from OnStar’s inception, huge leaps forward in technology have brought mobile networks, multi-touch screen dashboards and other things that consumers are used to on a tablet device to the fingertips of drivers.

In-car technology as an enabler for micro insurance.

Speaking of Hollywood – once fantastical gadgets reserved for James Bond’s vehicles are now very much a reality. Cars are increasingly being produced with exterior and interior cameras as standard, to aid drivers on-the-road and improve vehicle security. AI is also finding its way into the car – notably through assistants such as Apple’s Siri and Amazon’s Alexa – to assist the driver and passengers in real-time. Just don’t expect them to help you escape from a heavily guarded parking garage!

E-commerce is now in cars too – dubbed vehicle or in-car commerce in the automotive industry. Through a car’s dashboard system, consumers set up their payment information enabling them to make purchases for goods and services such as EV charging, fuel, and parking directly from their vehicle. This is of real benefit and an improvement in safety for drivers, who no longer need to use a smart phone at the wheel – or even leave their vehicle! – to make everyday purchases and links real-time location data to the services on offer.

Micro insurance is driven by data, analysis, and specified events. Connected cars are now collecting the types of data ideal for developing embedded micro insurance solutions, such as location, vehicle telemetry, image and video monitoring, and more! These data points can be used by claims handling AI to analyse and make informed decisions, providing drivers with real-time payments.

Representing a $230 billion commerce opportunity in the US alone, according to PYMNTS and P97 Networks, in-car commerce has the potential to become a major revenue channel for businesses – and this includes insurance.

What does this mean for retailers and micro insurance?

When purchases are made through a car’s dashboard, such as those mentioned earlier, embedded micro insurance can be used to enhance the value of the purchase – both for the retailer and customer. Micro insurance solutions provide an additional revenue stream for the retailer, while building customer trust and providing peace of mind that should the worst happen, enrolled customers are covered.

In the spirit of GM’s pioneering system, micro insurance can be applied to the automotive industry to offer convenient protections for vehicle security, driver safety, assistance with the cost of repairs, and protecting against on-the-road inconvenience. Let’s consider a few examples that could benefit from micro insurance.

Smart Camera Parking Protection.

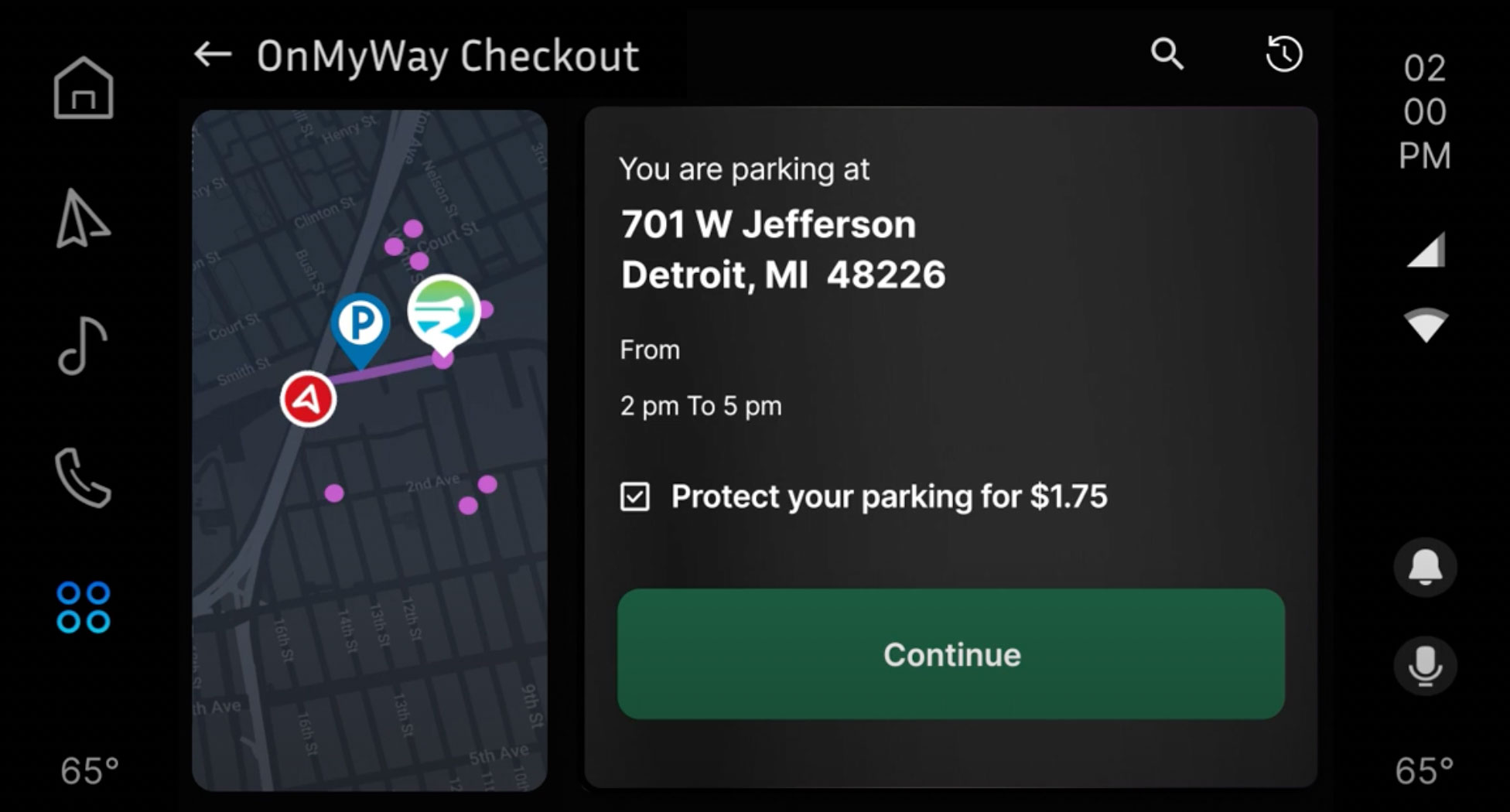

Anyone that drives a car has likely used a car park, purchasing a ticket for the duration of their stay. Drivers don’t know whether the car is completely safe, but it’s a risk that must be taken. Adding micro insurance to this transaction is one way to give drivers peace of mind over leaving their car – such as our recent partnership with Mavi.io’s OnMyWay Commerce platform. With the assistance of an integrated camera monitoring the vehicle – if a window is broken while the car is parked, the micro insurance product automatically provides an inconvenience payment for the driver to rectify the damages.

Source: Park & Protect with OnMyWay dash demo | YouTube

Missed Restaurant Reservation Compensation

Since transactions are completed through the car’s dashboard navigation system, new and innovative applications for micro insurance can be considered. Innovation & Tech Today reports that booking restaurant reservations is a popular theoretical use case in consumer surveys. Micro insurance could be applied to this transaction, providing protection for if the driver becomes stuck in traffic – through the combination of on-board navigation, traffic monitoring, and time keeping, inconvenience payments can trigger to soften the disappointment of a missed reservation.

AI Monitored Vehicle Servicing and Repairs

Cars need to be serviced throughout their lifetimes to ensure optimum performance. This wear-and-tear servicing is not generally covered by car insurance, so falls to the driver to pay as required. Car manufacturers are creating AI damage detection tools to aid drivers and mechanics with repairs and servicing, boosting driver confidence in the vehicle and productivity for the repairers. Micro insurance can hook into this data collection process, providing payments when the AI detects a fault or service due, enabling drivers to immediately afford repairs rather than delaying.

Sharing Economy Car Insurance

Micro insurance is also perfectly suited to peer-to-peer car sharing – and according to Turo’s director, was originally created for that specific purpose. Drivers who share cars on an occasional basis have no need for a yearly insurance policy, so micro insurance fills this gap by providing timed trip insurance. This ad hoc insurance is typically purchased via an app, though with the advances in connected-car technology, these transactions could be completed through the vehicle’s dashboard.

This example of P2P car-share insurance could be taken one step further. Cars used by multiple drivers could require users to log in to their personal insurance profile on a dashboard app to purchase or verify their trip insurance before the car can be engaged. This would provide security to the car’s owner and reduce the likelihood of uninsured drivers on the road, making travel safer for everyone.

In time, as built-in telematics sensors become available, it is expected that unique risk profiles can be generated for individual drivers, saved to their user profiles. This will enable tailored micro insurance policies to be offered to the driver, rather than basing the policy on the vehicle.

The In-car Commerce Opportunity

With in-car commerce representing such a large opportunity for revenue, it’s only natural for the insurance industry to look for ways to integrate and support new customers. This opportunity is not just revenue driven – there is also the chance for new micro insurance innovation. Connected in-car technology is collecting valuable data which can be used to develop inventive solutions to problems that inconvenience drivers every day. As in-car technology becomes more advanced and abundant, new partnerships with like-minded tech companies are a practical approach to enhancing drivers’ vehicle-based transactions.

Micro insurance is parametric in nature – triggered by specific events – and is purchased at a point of sales where it is often embedded with a relevant adjacent product giving access to insurance when needed rather than as a blanket coverage. Coupled with its convenience and affordability, this makes in-car commerce a prime untapped target for the micro insurance industry.

Contact us to see how MIC Global can help your business benefit its customers and employees with an embedded micro insurance solution, or simply send us your email address above to get started.