So, there we were, in a planning meeting, thinking about how to implement a parametric insurance product, how to fully secure and automate it….and then someone mentioned Hashgraph! What?????

Just as I was getting tired of hearing “blockchain this…” and “Lemonade that…” we now have “Hashgraph”….

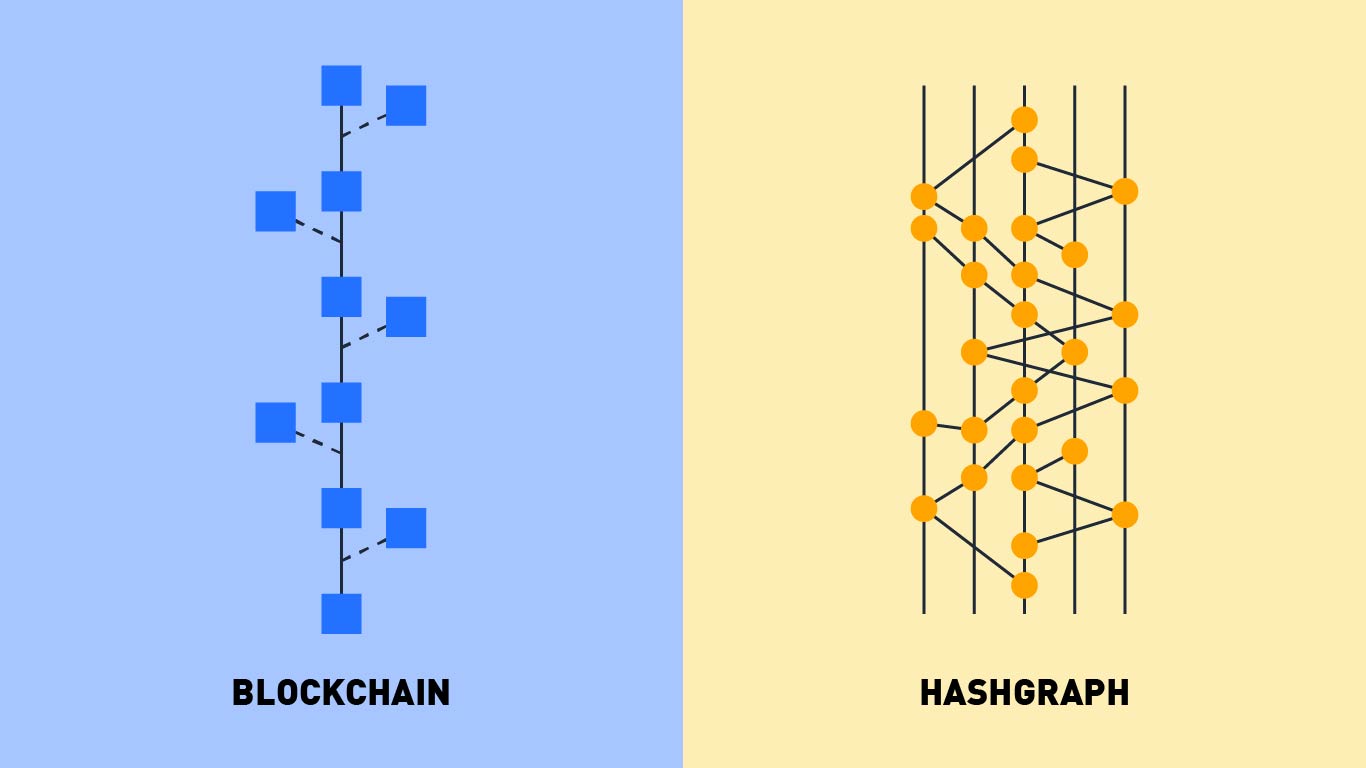

What is Hashgraph? Why was it so important to mention and for insurance?

Distributed ledger space is a huge talking point for insurance – smart contracts, security, cost reduction, trust – it all points to a move on to this tech. BUT blockchains come with limitations by design and are, by their nature, slow. By allowing the ‘community’ to come to agreement and throw away the blocks they don’t agree on speed suffers. In today’s world SPEED is king and this is a huge barrier.

Even in the slow paced world of insurance, how many applications are there that can just do 5 transactions per second? None, I think. Hence blockchains have been all talk, to-date.

Many large companies across sectors are increasingly testing blockchain PoCs, but full adoption is constrained by core limitations such as transaction speed.

The hashgraph algorithm, invented by Leemon Baird, the co-founder and CTO of Swirlds, is a consensus mechanism based on a virtual voting algorithm combined with the gossip protocol to achieve consensus quickly, fairly, efficiently, and securely.

YAY – QUICKLY – speed could be solved, and we can adopt.

“Hashgraph is an alternative to blockchain which is a first generation tech with severe constraints in terms of speed, fairness, cost, and security,” explained Mance Harmon, Co-founder of Swirlds and Hedera.”

For the layman what is Hashgraph? Well if you know what blockchain is (a distributed ledger technology) all about then this is relatively simple – Put simply it’s like Blockchain, but Hashgraph is without the limitations.

Under test, Hashgraph has performed well. Since time is a trade-off between throughput, latency, number of computers, and geographic distribution, the tests demonstrate these trade-offs very well without adding in another trade-off. For example, the results show 30 computers can achieve 50k transactions a second across 8 global regions in 3 seconds, or merely 1.5 seconds across 2k miles, or 0.75 seconds in a single region. This is great news and it could be time to open up PoC’s to this new tech.

These speeds mean that processors such as Visa can think of building it into their current network and transaction speeds.

The Hedera Hashgraph platform is architected to address the market of distributed applications. The vision provides an initial three sets of services as the platform evolves:

- Cryptocurrency as a service for support for native micropayments.

- Micro-storage in the form of a distributed file service that apps can use.

- Contracts.

Great – how do we play and pay? It works through a platform coin — when you make an API call to one of these three services, a micro-payment is made to the company.

The Hedera platform’s existing technical framework is capable of anti-money laundering and know your customer compliance which sits well for insurance. Regulatory compliance combined with enhanced security and speed could signal a time to start.

With a secure, fast, public ledger, the future could include micropayments and massive-scale distributed p2p insurance and other new models could be developed. Match distributed ledger technology and AI and the future is bright!

So, what to do now? We are looking at this tech to architecture our insurance models. We have been waiting until now owing to the fundamental issues in existing blockchain processes.